Changes To The Stage 3 Tax Cuts

The Stage 3 tax cuts, including stage 1 and stage 2 which were part of a packaged legislated in 2019 to address “bracket creep”. Both parties voted for the legislation and indicated that they would not change it in the 2022 Federal Election.

Bracket creep is a simple problem: as taxable incomes increase over time, taxpayers move to higher tax brackets and pay more tax as a percentage of their taxable income.

As an example, a taxpayer earning $75,000 in 2016 paid tax of $15,922 or 21% of his/her income. Assuming the same 2016 tax rates, that same taxpayer earning $92,756 in 2023 (increased by CPI only, and not performance) would have paid $22,267 in tax, or 24% of his/her income. The percentage of income paid in tax increased because the taxpayer’s earnings increased over time with inflation and he/she moved into a higher tax bracket. Bracket creep provides governments with increased taxation receipts and is a disincentive for taxpayers to earn more.

The Federal Treasury’s “Rethink” tax white paper produced in 2016 indicates “Australia’s individuals’ income tax regime is very progressive compared with other countries. Australia has relatively low average and marginal tax rates at low-income levels, but relatively high marginal tax rates at high income levels. Australia’s tax and transfer systems are highly progressive, which supports fairness. High effective tax rates, including as a result of targeting in the transfer system, can reduce participation incentives for some groups. Bracket creep exacerbates this problem.” Over time, unchecked bracket creep could potentially reduce workforce participation and the opportunities afforded to the community by higher participation rates.

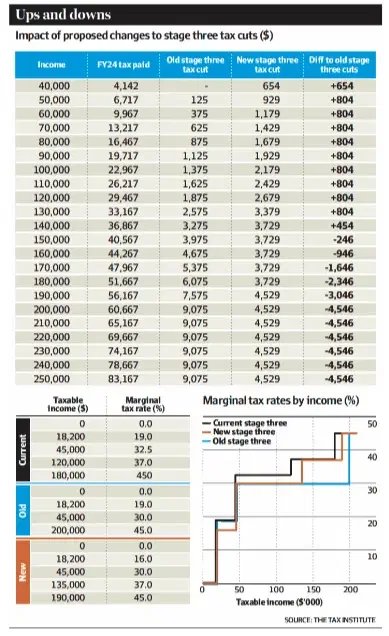

Last week the Government announced changes to the stage 3 tax cuts, in my view undermining the purpose of that legislation – addressing bracket creep. It reduced the amount to tax cuts originally legislated for higher income earners and increased amounts for lower income earners. The impact is summarised as follows.

Putting concepts such as honesty and integrity aside, the changes to the stage 3 tax cuts are a fabulous exercise in politics (likely increasing votes for the Government at the Dunkley and Cook by-elections this year and next year’s federal election). How can a change to the stage 3 tax cuts that places more money in the hands of more Australians not be a positive political move?

But it’s not necessarily a positive economic or taxation outcome. Paul Kelly in The Weekend Australian 27-28 January 2024 reports that “the bottom 40% of Australians pay no net tax. The top 10% of taxpayers will now pay about 47% of all income tax revenue. The top 5% of taxpayer paid about 32.9% of revenue in 2017-18, and under Labour’s plan, that will rise to about 34.6%. Economist Chris Richardson calculates that the top 1% pay as much income tax as the bottom 71%.”

The Weekend Australian also reports that in addition to the 2.1 million Australians who will receive a smaller tax cut because of the governments proposed changes, an additional 3.3 million are likely to pay higher income tax over the next 10 years, because of bracket creep.

In many countries around the world, tax brackets increase with CPI to avoid bracket creep. To achieve that in Australia will require tax reform, which will boost economic outcomes, which many bodies, including the OECD, have suggested we undertake. But that will require our politicians, of all persuasions, to act in the best interest of their country, it will require leadership and courage, and it will require excellent political skills. I am not certain that these requirements currently exist.

Peter Debus is a director at PrincipleFocus, a Chartered Accountant, Chartered Tax Adviser and a Graduate of the Institute of Company Directors.