NSW Tax Forum 2023 Key Learnings

The Tax Institute – NSW Tax forum 2023

The NSW Tax Forum is established as one of the premier taxation events in Australia and each year our team attends to ensure we are continuing to develop our knowledge and understanding. This year’s forum was attended by Pete, Kati, Audrey and Simon.

Designed by an organising committee made up of experts from the industry, the program addresses a variety of issues relevant to the profession and has something for every tax profession at every level. Kati has summaried the key learnings from highlight sessions for you:

Session 1: Division 7A – The things you didn’t know

Division 7A is an area of the tax law that private clients and practitioners in the private client space will generally have an awareness of. In particular, the core concept is that loans, payments and forgiveness from a private company to a shareholder or their associate can have adverse tax implications if not appropriately managed.

However, beyond an understanding of the core of Division 7A, there are many subtleties within the Division that can have material impacts on the tax outcomes that arise for the particular situation (and often in an adverse manner).

When is a repayment, not a ‘repayment’?

A payment must not be taken into account if:

(a) a reasonable person would conclude (having regard to all the circumstances) that, when the payment was made, the entity intended to obtain a loan or loans from the private company of a total amount similar to, or larger than, the payment; or

(b) both of the following subparagraphs apply:

(i) the entity obtained, before the payment was made, a loan or loans from the private company of a total amount similar to, or larger than, the amount of the payment;

(ii) a reasonable person would conclude (having regard to all the circumstances) that the entity obtained the loan or loans in order to make the payment.

Session 2: Selling a Business in a Trust when the Buyer Wants Shares in a Company

Potential options for sale by stakeholders in businesses carried on by trusts, be they discretionary trusts or unit trusts, to purchasers who wish to purchase shares in a company rather than purchase the business itself or the interests in the trust which carry on the business.

The reasons for considering a pre-sale restructure from a trust(s) to company(ies) and a subsequent share sale rather than a business sale include:

the business may be conducted, and business assets held, in a number of trusts. The purchaser may not wish to take the risk of entering into a complex transaction with potentially a number of parties and instead will require the vendor to undertake some pre-sale restructuring steps so that:

the business and business assets can be placed in a newly incorporated company or companies without history (NewCo);

shares in the NewCo or NewCos can then be sold to the purchaser;

a share sale rather than a business sale, particularly where part of the consideration will be scrip in the purchaser and therefore allow the vendor to access the Subdivision 124-M Rollover Relief.

Session 3: Trusts & UPE

Poor trust administration that causes problems

Problems will easily arise where there is a lack of clarity around the entitlements of beneficiaries and on what authority those entitlements have been dealt with/satisfied.

The common types of poor trust administrative practices that cause such lack of clarity include:

1. failure to advise beneficiaries of their entitlements each year – whether in writing or not, but of course in writing is preferred; and

2. failure to obtain the authority of beneficiaries – whether in writing or not, but of course in writing is preferred – for the non-payment of their entitlements, or for the payment (as satisfaction) of their entitlements to other persons or towards loans/goods/services for other persons.

At the extreme, circumstances may exist where trust distributions are practically regarded as being only “on paper” and not as creating entitlements requiring genuine beneficiary knowledge and direction in dealing with their entitlements. If not shams, such circumstances would invite consideration of section 100A.

ATO continues to suggest that if a trustee retains the UPE funds, then they must be used for working capital in a business, used to make investments or to lend to family members on a 7-year Division 7A loan basis.

Session 4: Superannuation and Estate Planning

The main reason for much of the litigation arising in relation to superannuation and estate planning is due to no documentation, faulty documentation or people not liking each other and trying to get a share of the pie to which they have no rights. Therefore, superannuation and estate planning are about documentation review, revision of documents review and constant revision to consider changed circumstances.

An effective way of ensuring benefits are paid as preferred by the deceased can be by the use of:

Binding death benefit nominations: This allows a member to make a decision concerning the distribution of death benefits in advance and effectively removes the ability of the trustee to determine who will receive the death benefit for dependants who are alive at the time of the member’s death.

Reversionary pensions: It can be a useful way of controlling the trustee’s discretion as they are paid automatically to the nominated reversioner and will occur without any involvement of the trustee.

Specially drafted trust deed provisions in relation to beneficiaries: Failure to review the deed may result in the unique provisions ceasing to be appropriate, for example, restricting the ability to rollover benefits to another fund.

Parties have separate SMSFs so that benefits and fund investments are isolated to a single member where disputes may potentially be on the horizon.

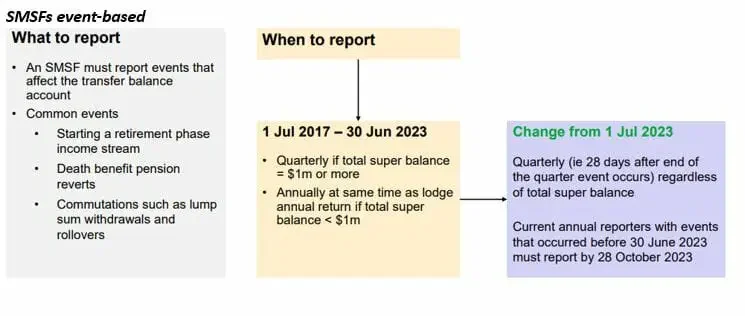

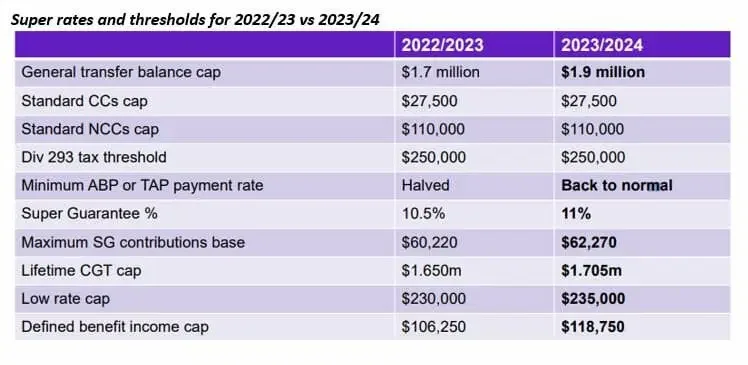

Session 5: SMSF update

SMSFs event-based

Super rates and thresholds for 2022/23 vs 2023/24

Session 6: Deceased estates with cross border issues

Global is the new normal:

Nearly 50% of Australians born overseas or have a parent born overseas

Foreign assets, relationships, residency and citizenship (even within the one family) are more likely and always create complexity in estate planning and tax

Multiple connections – consider which systems of law apply (succession and tax)

Careful planning needed to avoid cost and conflict

Given the complexities of the Australian tax and duties legislation, we have summarised a number of issues that commonly arise.

Determining tax residency: The first issue is to work out if the relevant individuals are Australian tax residents or not. This will be determined primarily by Australia’s domestic tax laws, as affected by the operation of DTAs entered into by Australian and other countries

Tax equalisation clauses: The Will could include provision for ensuring that the respective shares of the beneficiaries are adjusted to equalise the tax payable by the estate or to be paid from the share to which the non-resident beneficiary is entitled. This might not work in circumstances where there are insufficient assets from which to make the adjustment.

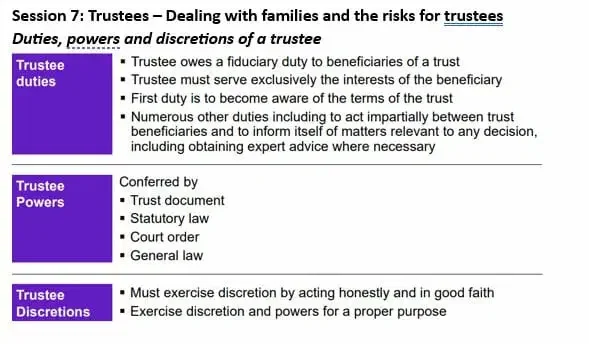

Session 7: Trustees – Dealing with families and the risks for trustees

Duties, powers and discretions of a trustee

Risk management tips for trustees

Seek advice from professional

Precedent advice letters

Bespoke trust deeds to cover particular family circumstances

Trustees should, in appropriate circumstances, seek expert advice (legal, tax and/or financial planning)

Regular contact/meeting with trustees to see if there are any ‘storm clouds on the horizon and take appropriate action

Be wary of clients asking you to act as co-trustees or as a director of a corporate trustee of a discretionary family trust – assert independence and legal obligations early

Decisions of trustees are not always black or white – difficult decisions advise trustees to approach the Court for appropriate orders or for judicial advice

This is not advice. Readers should not act solely on the basis of the material contained in this presentation. Items are general comments only and do not constitute or convey advice. Also changes in legislation may occur quickly. We recommend that formal advice be sought before acting in any of the areas covered in this paper.